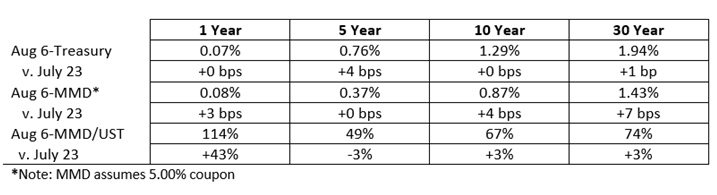

It is difficult to keep coming up with superlatives to describe the current tax-exempt market. We were involved in pricings this week for several different healthcare credits and everything from benchmark rates to credit spreads to covenant structures to investor participation was outstanding (at least from the seller’s side of the buy-sell equation). Even as the Federal Reserve begins to telegraph its intention to start tapering bond purchases, tax-exempt fund flows remain favorable, supply remains manageable, and transactions are seeing strong execution across different coupon structures. And the taxable side is still going great as well.

SIFMA reset this week at 0.02%, which is approximately 22% of 1-Month LIBOR and represents no adjustment versus the July 21 reset.

Better Enterprise Risk Management

Every two weeks I reference the amazing capital market environment; which makes me think about the magnitude of the U.S. central bank intervention that sits underneath it all; which makes me think about the possibilities from here and the fact that not a single person on the planet has any direct experience with any of it; which takes me back to the ideas put forth in a March 23, 2020, article in the Wall Street Journal by Allison Schrager where she used the initial crisis-stage COVID dislocation to offer a distinction between risk and uncertainty:

The future is unknowable, but risk is measurable. It can be estimated using data, provided similar situations have happened before. Uncertainty, on the other hand, deals with outcomes we can’t predict or never saw coming. Risk can be managed. Uncertainty makes it impossible to weigh costs and benefits…

Pair this with our “three phases of COVID” construct and the pandemic is a journey from the chaos of “uncertainty” (crisis) to stabilization to a place where once again “risk is measurable” (normalization). Unfortunately, the stabilization bridge between crisis and normalization seems to be as sturdy as one of those frayed rope contraptions in an Indiana Jones movie. The Delta variant highlights the issue, but there is a discouraging list of other uncertainty headwinds that are equally capable of making COVID stabilization a long and bumpy ride.

What seems to be happening is a blurring of the line between crisis and stabilization, which means that for the foreseeable future healthcare organizations will be surrounded by threats and uncertainties. If this is true, then any successful response will require embracing a new idea of risk management. Once again dating myself, Stanley Kubrick’s dark comedy about the threat of nuclear war between the U.S. and the Soviets (back when there were Soviets) was titled: Dr. Strangelove or: How I Learned to Stop Worrying and Love the Bomb. Change “the Bomb” to COVID (or maybe “Uncertainty” writ large) and we have the setup for the 2021 remake, which hopefully offers a happier outcome than Kubrick’s original tale.

Any sustained COVID stabilization initiative will be built on a functional enterprise risk foundation. This will not source naturally from the broad but shallow risk surveys used in most traditional Enterprise Risk Management (“ERM”) processes; traditional ERM and the idea of risk as a compliance or audit function will not help an organization navigate the dynamic turbulence that is going to define COVID stabilization. The need is for strategic risk management, which will come from identifying (and ultimately addressing) the risk subset that represents the major financial headwinds the organization confronts across operations, strategy, capital, and liabilities. If you have a legacy ERM infrastructure in place, the imperative is to retrofit it and find the subset of risks that represent systemic (not compliance) threats. If you haven’t done a broad ERM survey, then you should skip it and work on developing a bespoke risk roster. Either way, building a useful risk map requires that you:

- Identify the universe of key risks (or claims on organizational financial resources) that emerge out of your organization’s operations, strategic initiatives, capital investment, and liabilities

- Quantify each identified risk, which requires developing supporting methodologies, assumptions, and measurement parameters

- Quantify the timing and benefit associated with any dedicated risk offsets (commercial risk management products or internal credit resources) or management’s ability to react to risk

There is a subset of risks that are common to most healthcare providers and that generate material financial exposure, but even these more generic sector risks manifest in different ways; additionally, every organization carries a subset of risks that are unique to its circumstances and every organization has different expectations about its ability to offset or manage identified risk. Our experience has consistently shown that even if your organization has a similar risk profile to another organization, your functional risk map will not be the same. When you do the work, you generate a bespoke risk map that can adapt as your organization moves through time; can support more targeted risk management; and can open the door to a game-changing way of approaching resource deployment.

Unfortunately, “stop worrying and love COVID” is not going to work. What will work is positioning your organization to continuously understand and adjust the resource deployment balance between managing risk versus generating return. This balancing effort is always a healthcare financial management best practice, but right now it is also an imperative because the stakes of getting any of it wrong (managing risk, generating return, or balancing the relationship between the two) are incredibly high. Without any doubt the best way to do this is to pursue excellence in both strategic risk management (which is how you build a high functioning risk map) and strategic resource allocation (which is how you toggle the risk-return balance).

Trending in Healthcare Treasury and Capital Markets is a biweekly blog providing updates on changes in the capital markets and insights on the implications of industry trends for Treasury operations, authored by Kaufman Hall Managing Director Eric Jordahl.